What is Title Insurance?

Title insurance is an important cost component within Closing Costs that always intrigues a first time home buyer. Title insurance in North Carolina protects buyers and lenders from financial liabilities that may arise due to a title defect or a hidden lien.

Have a look at our Title Insurance explainer video to see how title insurance can protect your lender and your ownership in case of a title defect.

There are two types of North Carolina title insurance policies: Lender’s Title Insurance Policy and Owner’s Title Insurance Policy.

Lenders in North Carolina often require borrowers to purchase a North Carolina Lender’s Title Insurance Policy which guarantees protection for North Carolina lenders against issues arising out of defects on the title of a North Carolina property. On the other hand, the North Carolina Owner's Title Insurance Policy protects the buyer against claims and liens.

Title insurance policy premiums in North Carolina show up as line items within a closing cost worksheet for a buyer and seller such as a Closing Disclosure, Loan Estimate, HUD-1, or an ALTA Settlement Statement. If you're looking to get a preview of what these costs look like, use this free North Carolina title insurance calculator.

How much does Title Insurance Cost in North Carolina?

North Carolina title costs are on the lower side as compared to other states with a lot of real estate activity.

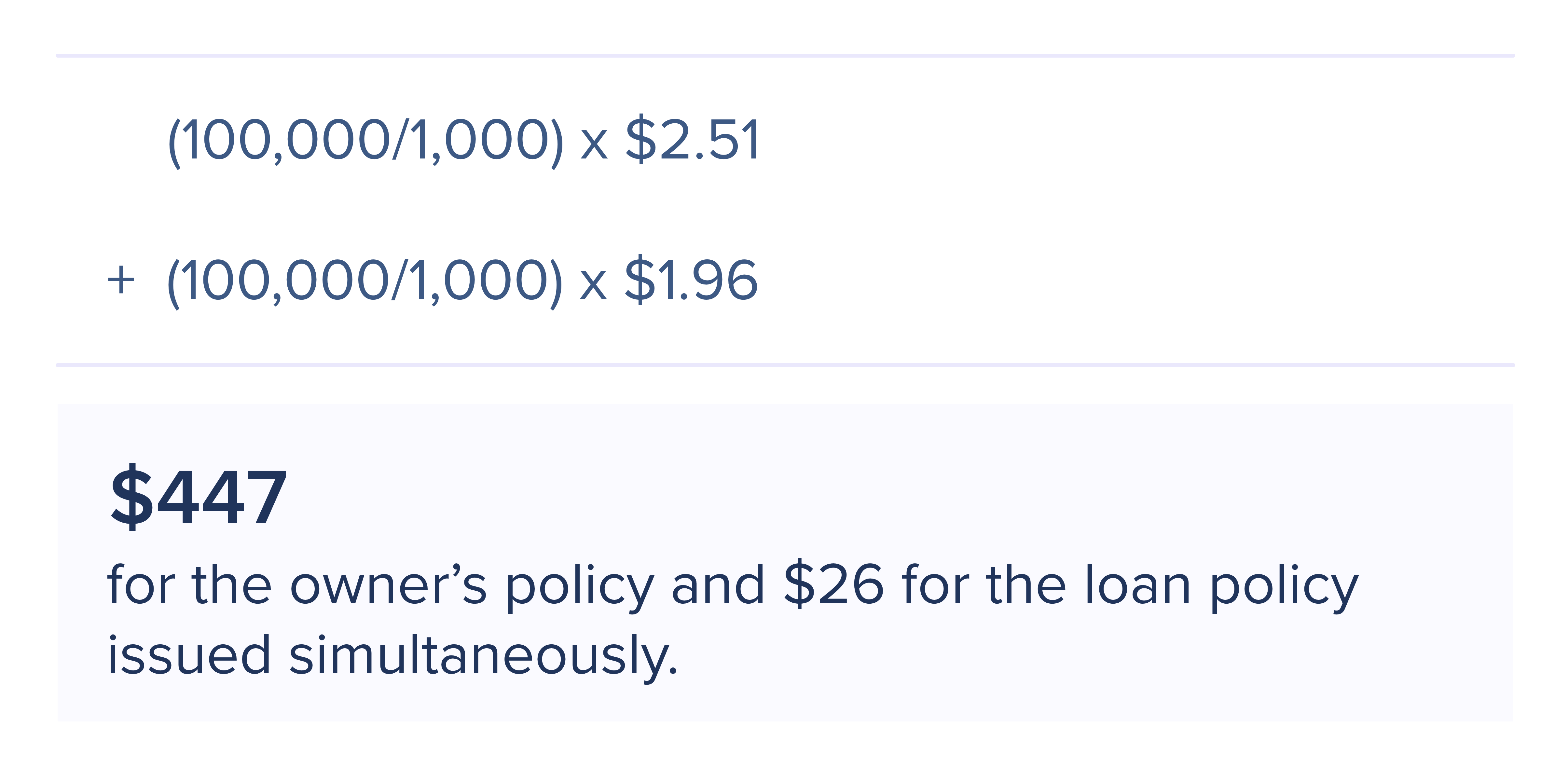

A property of $200,000 will cost you $447 for an owner's policy. On the other hand, a flat $26 is charged for the lender's policy on each mortgage, bringing up the total to $473.

Please note, these costs are excluding any endorsements, closing services, or liens. If your property needs any endorsement, it will add to more costs.

Here are a few more use cases:

To give a perspective, these 3 use cases give you a complete idea of what to expect when closing in North Carolina.

- For a purchase price of a $250,000 property in North Carolina with a 20% down payment ($70,000), the cost of title insurance policy and lender's policy are $545 and $26 respectively.

- For a purchase price of a $250,000 property in North Carolina bought with full cash, the cost of the title insurance owner's policy is $545.

- For a purchase price of a $500,000 property in North Carolina with a 20% down payment ($100,000), the cost of the title insurance owner's policy and lender's policy are $1,035 and $26 respectively.

- For a purchase price of a $500,000 property in North Carolina bought with full cash, the cost of the title insurance owner's policy is $1,035.

- For a purchase price of a $1,000,000 property in North Carolina with a 20% downpayment ($200,000), the cost of the title insurance owner's policy and lender's policy are $1,615 and $26 respectively.

- For a purchase price of a $1,000,000 property in North Carolina bought with full cash, the cost of the title insurance owner's policy is $1,615.

How to Calculate Title Insurance Cost for North Carolina?

There are 5 cost brackets or slabs that you should take into account to calculate the total title insurance cost for your property. These are:

| Property Cost | Rate |

| Up to $100,000 | $2.51 |

| $100,001 to $500,000 | $1.96 |

| $500,001 to $2,000,000 | $1.28 |

| $2,000,001 to $7,000,000 | $0.98 |

| $7,000,001 | $0.68 |

Say you want to calculate the cost of the owner's title policy for a $200,000 property. The total cost would be:

What is Lender’s Title policy in North Carolina?

The lender’s policy is often purchased along with the owner’s policy. It protects the lender from title defects such as a pending construction lien on the property, errors in the title, and other issues that may arise after the title has been transferred to the buyer.

What is the Owner’s Title policy in North Carolina?

The owner's policy is a legal document that shields the owners from unknown defects such as missing heirs, incorrect documentation, unjust court proceedings, and protects their ownership. The owner’s policy constitutes the major share of the title insurance cost.

What is not covered in Title Insurance in North Carolina?

Title insurance may not cover the following:

- Damage due to a fire

- Infestation

- Financial losses due to inadequate property inspection.

- Damages due to natural calamities such as thunderstorms.

How long is the title policy valid in North Carolina?

The title policy remains valid till the time you remain the owner of the property. Only when you decide to sell, a new policy must be made in the name of the buyer. The lender’s policy is valid till the mortgage is paid back.

Who regulates Title Insurance prices in North Carolina?

The North Carolina Department of Insurance is responsible to hand out licenses to title companies and also decide and monitor the charges levied by these title companies in the state.

Who pays the Title Insurance in North Carolina?

The North Carolina Department of Insurance has laid some rules on the distribution of the amount paid for title insurance. Title insurance costs are often divided between the seller and the buyer in North Carolina. Costs that are covered by the buyer include:

Earnest Money Deposit. An amount paid to the listing agent or the closing attorney. It is also called the token money many times and it is refundable if the buyer backs off from the deal.

Due Diligence Fee. It is paid to the seller to help them start the underwriting process and initiate home inspections. This amount is generally is non refendable.

Other Fee. In addition to the fees listed above, the buyer is also supposed to pay for a termite inspection, well/water inspection, septic tank inspection, etc.

On the other hand, the seller paid costs can include the following:

- Real Estate Commissions

- Revenue Stamps

- Recording Charges

- Document Preparation

- Mortgage Payoff

- Property Taxes

Is Title Insurance required in North Carolina?

Title insurance is a must have for every buyer buying properties across North Carolina. This is because the land and the property may have various rights that might be diversified across multiple owners. For example, if property taxes are pending for the property, the government can have a lien against it without the new owner ever knowing about it.

This is where the lender's policy safeguards the lender from such discrepancies that are revealed during the title search.

Additionally unknown defects such as missing heirs, incorrect documentation, unjust court proceedings, etc. can also pop up that do not show up in the title search. This is where the owner's policy shields the owners and protects their ownership.

This is why it is always best to go for title insurance irrespective of the fact that it is mandated by the state or not. It does not take more than 4-5 days to get the title commitment back from the seller and be sure that the property has no impending liens.

Should you shop for title insurance in North Carolina?

You can definitely shop for title insurance in the state of North Carolina by approaching any reputable title company. However, if you are skeptical, you can ask your agent or lender to help you out with the process.

How does Title Insurance work in North Carolina?

The title insurance protects your ownership in the event of a title dispute arising from claims, title errors, encumbrances, and much more. In these cases, the title company will pay for any losses incurred due to title defects that did not appear during the title search process. In addition to that, the title company is also bound to defend your ownership of the title and should pay the legal expenses to do that.

Is there any discount on Title Insurance Policy in North Carolina?

Technically there is no discount on title insurance in North Carolina. But what you can do is go for simultaneous issuing of both Owner’s Policy and Lender’s Policy at the same time. This way you only pay a fixed amount for the Lender’s Policy.